When a motor vehicle is involved in an accident and requires a tow, insurance carriers, service providers, and body shops all have essential roles to play. Importantly, these parties need to work together to ensure that the vehicle is recovered and repaired as quickly and efficiently as possible. When challenges arise that impact the operations of one party, it hinders the entire process, leading to longer repair times that are more disruptive to the policyholder and increase claims costs for the carrier. One example of this is in the event of a body shop refusal, which refers to a situation where a body shop must refuse delivery of a vehicle that is being dropped off for collision repair.

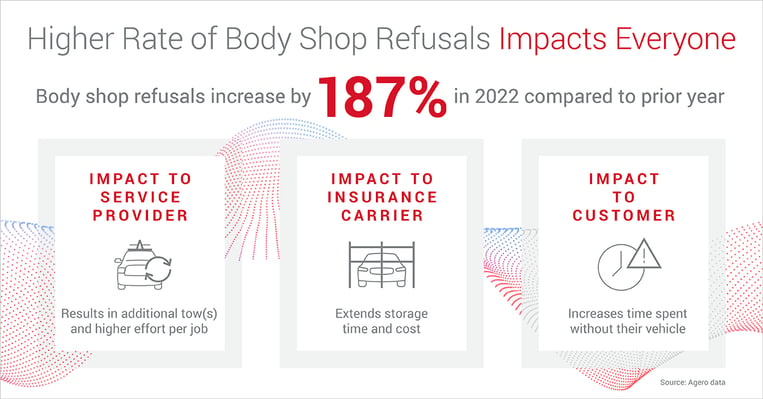

Body shop refusals have been a problem for years, and recently, the rate of these events (and their impact) has been rising steadily.

As a partner to all of the impacted parties, Agero broke down the factors driving the increase in body shop refusals, as well as some tactics we can use to address this challenge.

Three factors driving the increase in body shop refusals

The increased frequency of body shop refusals after an accident can be traced to macro challenges such as increased volume, parts shortages, and labor shortages, as well as changing dynamics within the accident management ecosystem.

Parts and storage shortages + high demand = low capacity

We’ve reported in the past about how driver behavior has changed over the past few years, leading to a higher number of accidents as well as an increase in accident severity. More accidents leads to more volume for body shops, which, in turn, drives up their demand. As vehicles continue to arrive faster than shops can repair them, storage limitations restrict shops from accepting new vehicles.

Adding to that is the all-too-familiar issue of parts shortages. Lingering supply chain issues have created serious parts shortages that prohibit body shops from repairing vehicles quickly. This leads to extended storage times and leaves insurers and consumers with a higher storage bill.

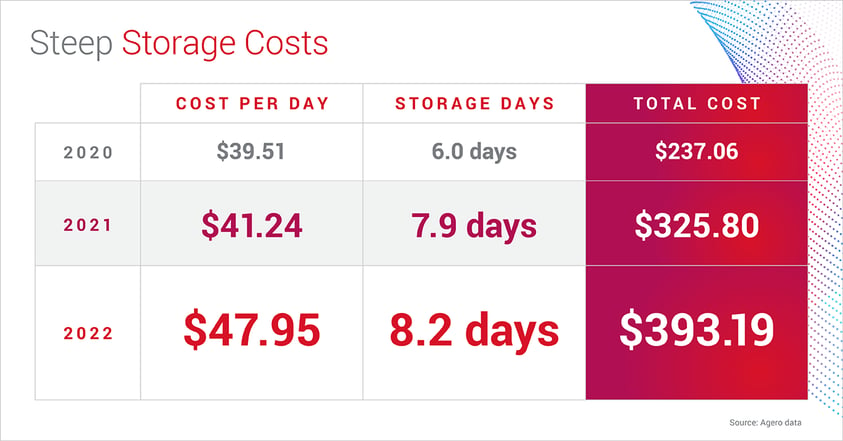

High storage costs are further driven by the impact of inflation. With storage rates increasing by 21% since 2020, auto insurers are hit hard each time a vehicle is refused at the body shop.

Lack of Communication Between Carriers and DRPs

As insurance carriers feel the impact of rising costs, they’re pushing harder on their shops with Direct Repair Programs (DRP). These shops have contractual agreements to prioritize vehicles insured by certain carriers. According to CCC Intelligent Solutions, the majority of DRP participation and volume belongs to national Multi Shop Operations (MSOs) who have multiple facilities that specialize in different types of repairs.

However, when a front-line rep for an insurance carrier selects which shop a vehicle should be delivered to, they are oftentimes unaware of what type of repairs that shop may specialize in. As a result, the body shop must refuse that vehicle simply because they are not equipped for that specific repair.

Additionally, since the majority of DRP appraisals are sent to national MSOs, their capacity is restricted even further, leading to longer repair times and backlogs that are at an all-time high. Since the capacity at a given shop is rarely confirmed before the vehicle is delivered, a trend emerges where vehicles are continuously sent to shops that have no availability, resulting in repeat refusals at that location.

Hiring and training challenges create delays

With historically low unemployment rates driving high competition for workers nationwide, many carriers are facing staffing issues. In fact, claims roles are currently facing the highest turnover rate in the industry. These staffing challenges lead to slower appraisals. This means the shop is then required to store the vehicle until they receive approval from the carrier, thus taking up precious storage space and limiting the shop's ability to accept other vehicles.

Repairers are facing similar challenges. According to the 2022 FenderBender Industry Survey, 34% of shop owners reported a shortage of qualified technicians to be a serious challenge. Additionally, new vehicles are fitted with more sensors, cameras, and other tech that makes the vehicle smarter, but also increases the repair complexity, leading to additional training requirements that add to repairer’s labor challenges.

What can auto insurers do to improve the situation?

With so many factors feeding the rising trend of body shop refusals, increased collaboration from all ecosystem players is essential. As a central component to the process, the insurance carrier has an opportunity to bridge some of these gaps.

For starters, understanding the challenges that the body shops are facing can create a more collaborative and empathetic relationship between the two. Since the primary factor is high capacity (which is expected to linger for the foreseeable future), insurers should seek to improve how they interoperate with their shops as a long-term fix, rather than asking body shops for faster repairs on a case-by-case basis.

A few pre-dispatch confirmations by the insurance associate could also help the situation. Insurers should examine their current shop assignment process and ensure that their associates are verifying shop capacity. By confirming the shop’s capacity and which jobs they’re capable of repairing, the agent can select the best body shop for the job and reduce the chances of the vehicle being refused.

We’re in this together

Addressing the challenge of body shop refusals will not happen overnight. Given the interconnected nature of this ecosystem, it will require collaboration and a data-driven approach to overcome these market distorting forces and improve the process for all involved. In the meantime, reach out to Agero to see how we can assist with analyzing your body shop refusal rates and identify regional trends.

As Product Marketing Manager for the Accident Management line of business, Jake Wright is responsible for positioning, marketing, and go-to-market activities for Agero’s accident management products. Prior to joining Agero, Jake built and supported marketing initiatives in industries ranging from craft brewing, to telecommunications, to oil and energy. His experience in Product Marketing stems from a passion for learning and using creative problem solving to market complex products. Based in Boston, Jake is an avid sports fan who enjoys traveling, golfing, and skiing. Jake has a BS in Business Administration from Plymouth State University.

As Product Marketing Manager for the Accident Management line of business, Jake Wright is responsible for positioning, marketing, and go-to-market activities for Agero’s accident management products. Prior to joining Agero, Jake built and supported marketing initiatives in industries ranging from craft brewing, to telecommunications, to oil and energy. His experience in Product Marketing stems from a passion for learning and using creative problem solving to market complex products. Based in Boston, Jake is an avid sports fan who enjoys traveling, golfing, and skiing. Jake has a BS in Business Administration from Plymouth State University. Recent Posts

Agero Launches Sixth Annual ‘Summer Hustle’ Program to Honor Top-Performing Roadside Assistance Providers

Program celebrates the service professionals who help keep drivers safe and supported during the...Driving the Future of Roadside Assistance: Agero’s Momentum and the Road Ahead

As a leading provider of roadside assistance across North America, Agero supports more than 150...Agero’s Beth Davidson Wins 2026 BostonCMO ORBIE® Award

Recognition marks rare ORBIE triple crown for Agero with award-winning CMO, CIO and CISO.MEDFORD,...